Remitly S-1 Filing

Customer economics, founding story, growth strategy

Founding Story

The inspiration behind Remitly came when Matt Oppenheimer, the founder, was working for Barclays in Kenya and saw how difficult it was to send and receive money overseas, but his problem was more concerned with Swift and wire transfers. But what we saw with his Kenyan friends was that their livelihood came from remittances. 70-plus per cent of remittances were for basic living expenses with an average transaction size of $250. And that money went way far in people's lives.

They wanted to transform remittances, but didn't start out with building Remitly out of the gates.

Pivot

In the very early days, they started out by building the first "search engine for remittances," to help bring more price transparency to the industry like Kayak, the meta-search travel website. A metasearch engine or website lets travellers compare hotel room rates from various online travel agencies (OTAs) and other booking sites all in one place.

It turns out that it was not the best model to transform remittances because there was no business model because when you build top-level trust with the customer, meaning this service or option will safely send money from one country to another, you can't pass that to some other service provider. So they rejected the solution just by talking to people, so it was a pre-product, didn't build anything.

Remitly (The Company)

So they pivoted to become the actual money transmitter with the vision

"Transform the lives of immigrants and their families by providing the most trusted financial services on the planet".

They started the company in May 2011 in Seattle but didn't do their first transaction till April '12 since remittances are highly regulated, and they had to wait to get their first license in the State of Washington, which they acquired in April 2012. Hence, it took them almost a year to do their first transaction. That was also only focused on Washington State to the Philippines; they literally started with one country and one state.

And for the first 3 to 4 years in 10 years and five months of company history, they just did remittances from the US to the Philippines. Primarily because one sending money sounds easy, but it's hard, second they wanted to get their product right by learning from their customers before they start thinking about expanding to new currency pairs, and third limited resources.

They rented a booth in a mall in front of a remittance centre very early on, with the primary focus on learning from customers visiting the remittance centre. They knew this wouldn't make a huge impact on growing the customer base, but it was a perfect way to learn from customers, leverage their feedback and iterate on the product.

Remitly Flywheel

As customer base increases and customers complete more transactions, Remitly collect more data. This data enables Remitly to refine their marketing strategy, improve the customer experience, and accelerate the pace of launching new services for customers, or for the recipient.

Having this broader suite of services/products attracts more customers and enhances the experience further, which drives more transactions to Remitly and fuel further compounding organic growth.

But the core is the trusted experience and not just for the first time but for the every subsequent time and for both new and existing customers. If that trust degrades everything else falls apart.

Product

Remittance Product | Passbook | Remitly for developers

Remittance Product

Remitly can disburse remittances to more than 3.5 billion bank accounts, over 630 million mobile wallets and alternative payment methods, and over 355,000 cash pickup locations (including retail outlets and banks) in more than 115 countries.

And has direct integration with 100 partners around the globe. This enables them to settle transactions as fast as possible. In 2020, 75% of all total transactions were completed in less than one hour.

Passbook

Remitly launched Passbook in partnership with Sunrise Bank N.A. (“Sunrise”) in 2020. Passbook is a digital banking service designed specifically for immigrants. This is the first step in developing broader suite of products/services on top of the remittance product. Building on top of the remittance product can drive marketing synergy with the remittance product enabling more efficient customer acquisition for Passbook and for future products as well.

While Passbook is still in early stages, Remitly believes that, over time, they will be able to utilize the data and insights gathered from the remittance customers to tailor meaningful financial services for the needs of immigrant customers, and will give Remitly broad access to shared revenue and fees from the bank partners to whom these financial services are marketed.

And diversify the revenue base across multiple products serving the same core customers.

Remitly for developers

In 2020, Remitly launched Remitly For Developers for its business customers. A remittance-as-a-service offering that leverages their custom-built global network and compliance and regulatory infrastructure. With Remitly for Developers, businesses and their developers can integrate this network and infrastructure into their existing applications and websites through APIs, offer digital cross-border remittances to their customers, and introduce new digital banking solutions in emerging markets.

Market

Remitly is going after the two of the largest financial services in the world, one cross-border remittance and the other banking.

The cross-border remittance market alone is estimated to be approximately $1.5 trillion in total migrant remittance inflow volume in 2020 (including both formal and informal person-to-person channels) and generates over $40 billion in transaction fees globally and $540 billion formal remittance flows to low- and middle-income countries.

TAM = $1.5 trillion

SAM = $540 billion

Present (Annualized 2021) = $18.5 billion (18.498)

That’s 1.23% of the $1.5 trillion and approximately 3.42% of the $540 billion core serviceable available market. Ton of scope to grow in remittances.

Business Model

For the core remittance product, which also represents the vast majority of the revenue, revenue is generated from transaction fees charged to customers and the foreign exchange spreads.

And transaction fees vary based on the

corridor,

the currency in which funds are delivered to the recipient,

the funding method a customer chooses (e.g., ACH, credit card, debit card, etc.),

and the size of the transfer.

Corridor: is the pairing of a send country, from which a customer can send a remittance, with a specific receive country to which such remittance can be sent. US to India is one corridor and US to Australia is another corridor.

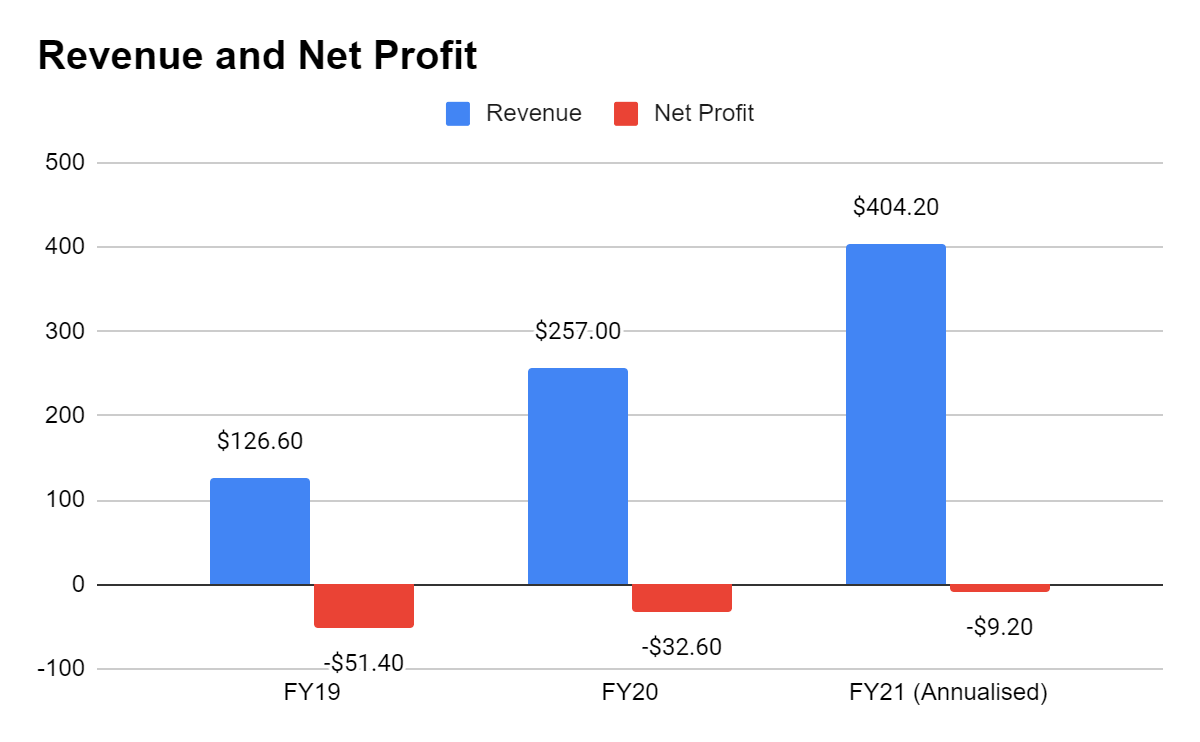

For the fiscal years ended December 31, 2019 and 2020, Remitly generated revenue of $126.6 million and $257.0 million, respectively, representing year-over-year growth of 103%. And incurred net losses of $51.4 million and $32.6 million, respectively, for those same years.

For the six months ended in June 30, 2021, Remitly generated revenue of $202.1 million and incurred net losses of $9.2 million. Annualised revenue rate = $404.2 million and growth rate of 57.27% YoY.

United States contributes the most revenue. Revenue from the United States represented $199.0 million for the year ended December 31, 2020, which was 77% of total revenue for the year.

Customer Economics

In 2020 Remitly completed approx 31 million transactions (30.6 million). For three months ended at Dec '20, they had 1,891,000 (1.89 million) active customers, assuming this number for the whole year (2020).

Remitly's customers did 16 transactions/year on average. (30.6/1.89 = 16.18). That means customers use Remitly more than once every month.

And with an average transaction size of around $394 in 2020. ($12.1B/30.6m). Every customer sent around $6374 in 2020.

ARPU is around $135.88 (Revenue/active customers at Dec’20). And CAC was around $78.26 (Marketing spend’20/change in #active customers).

Customers generally send money from the US, Canada, the United Kingdom, countries in Europe, and Australia —> to India, the Philippines, and Mexico.

Remitly defines active customers as distinct customers who have completed at least one transaction during the time period concerned.

“Active customers” is defined as the number of distinct customers that have successfully completed at least one transaction using Remitly during a given calendar quarter. We identify customers through unique account numbers.

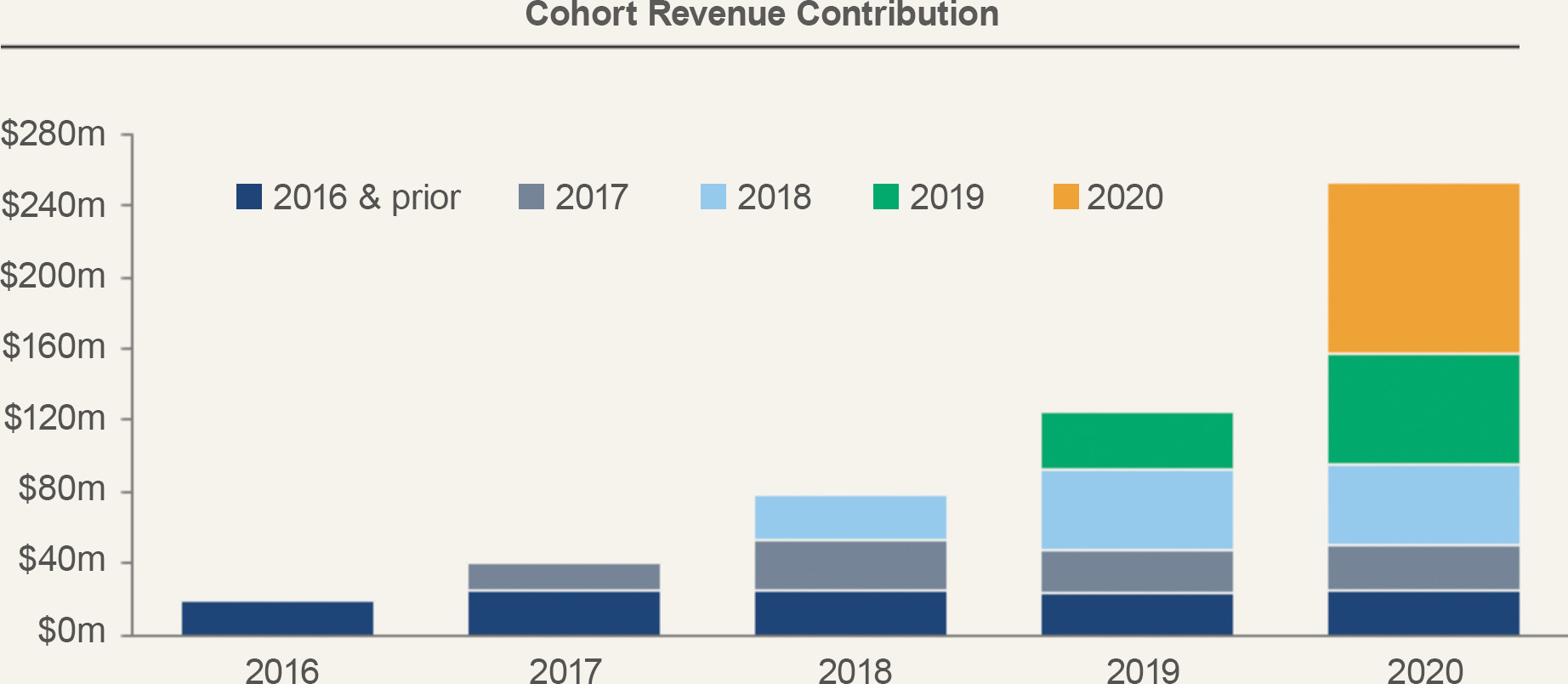

The chart below shows annual revenue contributions from customer cohorts acquired during a particular year ended December 31. And cohorts typically retain over 90% of the revenue generated in the preceding year.

Remitly has overall payback period of approximately 10 months. The five-year LTV/CAC ratio was greater than 6x for customers acquired during the year ended December 31, 2019. Representing an estimated 5-year LTV of $195.1 million divided by a CAC of $29.7 million.

Long Term Growth Strategy

The key elements of Remitly’s long term growth strategy according to the S1 filing:

Gaining share in existing corridors

Growing the customer base by expanding the marketing efforts across existing corridors to increase brand awareness with customers and highlighting the value of Remitly’s product. As Remitly grows their customer base, they expect to benefit from increased operating leverage in the business and more data and insight to enhance the models.

◦Increasing customer engagement and driving repeat use by developing new features to tailor and personalize our customers’ experiences and continue by continuing to add establish new disbursement partnerships and new payment methods to enhance the cross-border payment remittance experience for current and potential customers in the existing corridors.

Expanding to new corridors and partner networks by increasing the reach to thousands of additional corridors and growing the number of disbursement, payment and other partners and increase the number of direct integrations with such partners. This also provides an opportunity to not only expand the remittance business but also Passbook and Remitly For Developers.

Continue expanding into broader financial services by catering to the needs of immigrants. For example, the Passbook app started with deposit services, but will expand to new products and features within the app in order to provide solutions to a broader array of our customers’ problems.

Pursue strategic partnerships and acquisitions to accelerate growth objectives or to enhance the competitive position within existing and new products and markets. For example, in March 2021, Remitly extended the partnership with Visa and integration of Visa Direct1 within the global network, providing customers with real-time cross-border payments options to more countries around the world.

Operating Leverage is a measure of how revenue growth translates into growth in operating income and is calculated as FixedCost /Total Cost.

Remitly <>Vertical Fintech

Vertical Fintech: Over the last year or so, various startups have launched that are serving the needs of specific market segments — whether that is an industry, life stage, or demographic. Thanks to this strong focus on a niche, they offer a better proposition than incumbents/horizontal players. And as they scale, they cross-sell additional products.

Fun Fact: Bank of America got its start catering to the Italian-American immigrant community.

Some Examples

Tenth aims to erase the wealth gap for Black Americans, Crediverso provides financial products for the Hispanic community, and Squire offers back-end financial management software for independent barbers, for example.

Juni, a neobank for anyone buying media online, enables its users to get 1% back on every dollar spent on Facebook Ads and Google Ads.

Karat, a fintech startup, launched a credit card for online creators. Their aim is to build better banking products for the creators who make a living on YouTube, Instagram, Twitch and other online platforms.

Remitly is also working on the same lines. Their customer segment is immigrants. Such startups/companies might have a smaller TAM but benefit from:

Laser-focused messaging and natural network effects → lower CAC

Viral adoption within communities and strong word of mouth → strong organic growth

Strong community and mission alignment → low churn / strong retention

High engagement and customer buy-in → more likely to become “primarily financial institution” → successful cross-sell and higher ARPU

Additional reads on vertical fintech: Redpoint Ventures | A16z | Vertical Neobank

Thanks for reading 😀